Updated

Masan High-Tech Materials Advances Its Global Strategic Materials Platform Through Partnership with GB Innovation

July 09, 2026

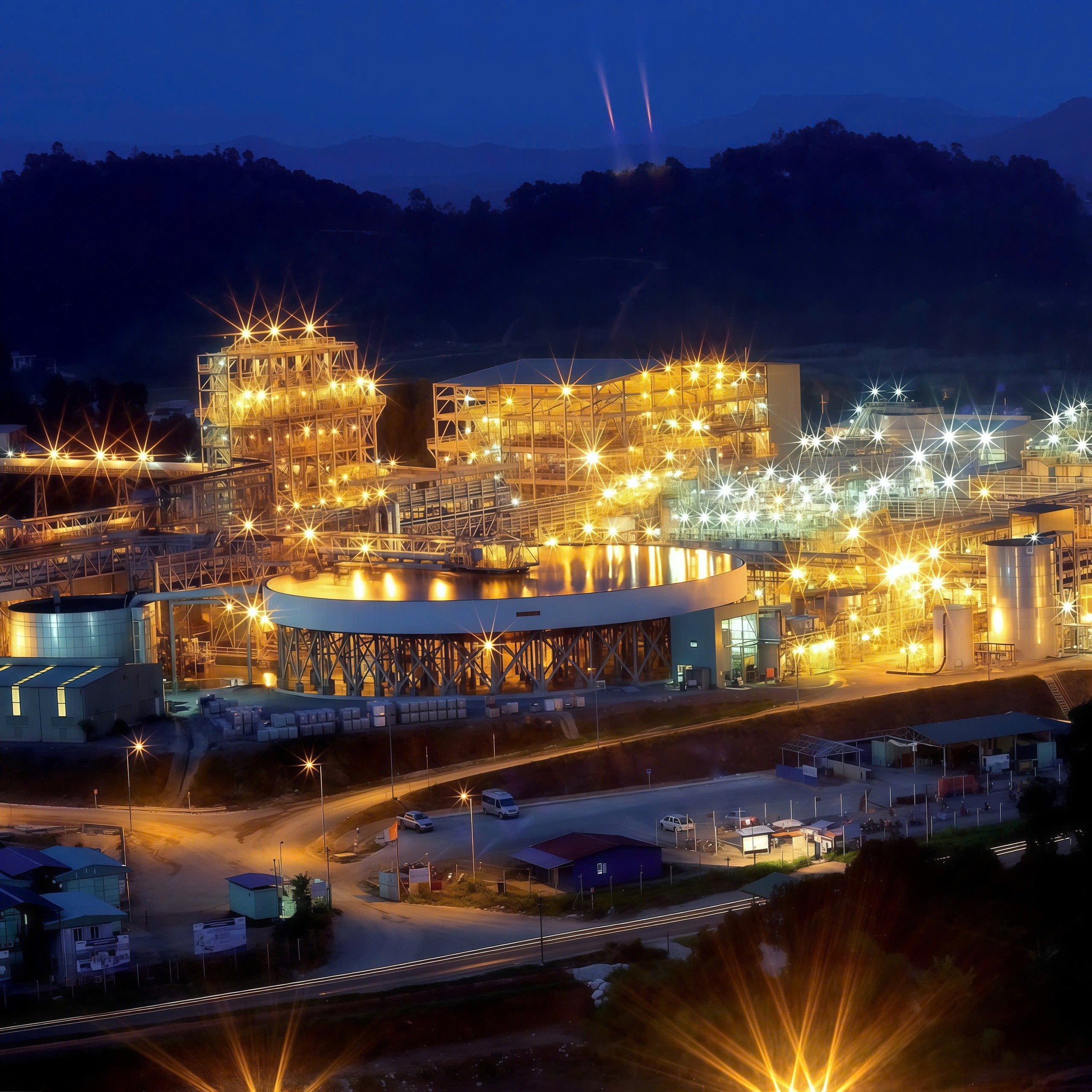

“Critical minerals are no longer a supply chain footnote, they are the new battleground for technological innovation and national security. MSR is not a mining company. It is a scarce tungsten materials platform that powers the supply chain for AI chips, defense systems, and precision manufacturing. Tungsten deposits are finite and irreplaceable, the strategic value only compounds over time. MSR is a strategic global asset positioned to generate strong cash flows”, said Danny Le, CEO of Masan Group.

Key Highlights:

In 1Q2026, MSR delivered net revenue of VND2,993 billion, up 114.9% YoY, and record quarterly NPAT Post-MI of VND537 billion. 2Q2026 profit is expected to increase QoQ, putting MSR on track to meet or surpass its FY2026 guidance of VND20,300 billion in revenue and VND2,500 billion in NPAT Post-MI, while targeting Net Debt-to-EBITDA below 1.7x by year-end. Tungsten prices have re-rated to over USD3,000/mtu, up 700% over the past twelve months, supported by aging mines, declining grades, long development lead times, high capital intensity, tighter Chinese exports, broadening strategic demand and low substitution risk. Rising geopolitical uncertainty, Western stockpiling and demand for secure critical-materials platforms further reinforce tungsten’s security-of-supply premium. Assuming APT prices average above USD1,500/mtu, MSR targets Net Debt-to-EBITDA of approximately 0.1x by end-2027 and a net cash position by end-2028, positioning MSR to become a stable cash-flow platform with dividend capacity.